Can Public Banking save the Financial System and prevent Consolidation and a Credit Crunch?

On Fox Business, Shark Tank’s Kevin O’Leary touted North Dakota’s remarkable pro-growth environment with the Nation’s fastest growing GDP per capita. While O’Leary praised North Dakota for its pro-business policies and oil and energy production, he also praised the State for its sovereign public bank, which may seem antithetical for a Reaganite Conservative. Kevin O’Leary deserves scrutiny for being a paid spokesman for FTX, after previously calling crypto garbage, but it is nice to hear a pro-business conservative make a free market case for public banking. O’Leary, who opposed the bank bailouts, considers public banking, a more fiscally responsible alternative to putting the tax payers on the line for reckless banking decisions and moral hazard. There is also much less risk of bank runs, than with fractional reserve banking, where banks are only required to hold a fraction of deposits.

There is irony in how some of the strongest populist policies are in conservative Red States like North Dakota, which also has restrictions on mega corporations owning agriculture, much like Alaska’s citizen dividend from oil extraction. On the other hand, the leftwing Jacobin, had an op-ed in support for public banking, granting credit to founding North Dakota’s Public Bank, in 1919, to a leftwing farmers movement. This movement was in response to wheat farmers being preyed upon by private bankers, with the objective of creating a bottom up economy, where the common man could have access to credit, and not be reliant upon Wall Street. Though this left-populist, localist, agrarian, movement, including the Non-Partisan League, were very different from what is considered leftwing today. Overall, there is crossover support for public banking, besides Reagan Conservative, Kevin O’Leary, including the leftist site Jacobin, and Ellen Brown and economist, Michael Hudson, proponents of public banking, in that early 20th Century populist tradition.

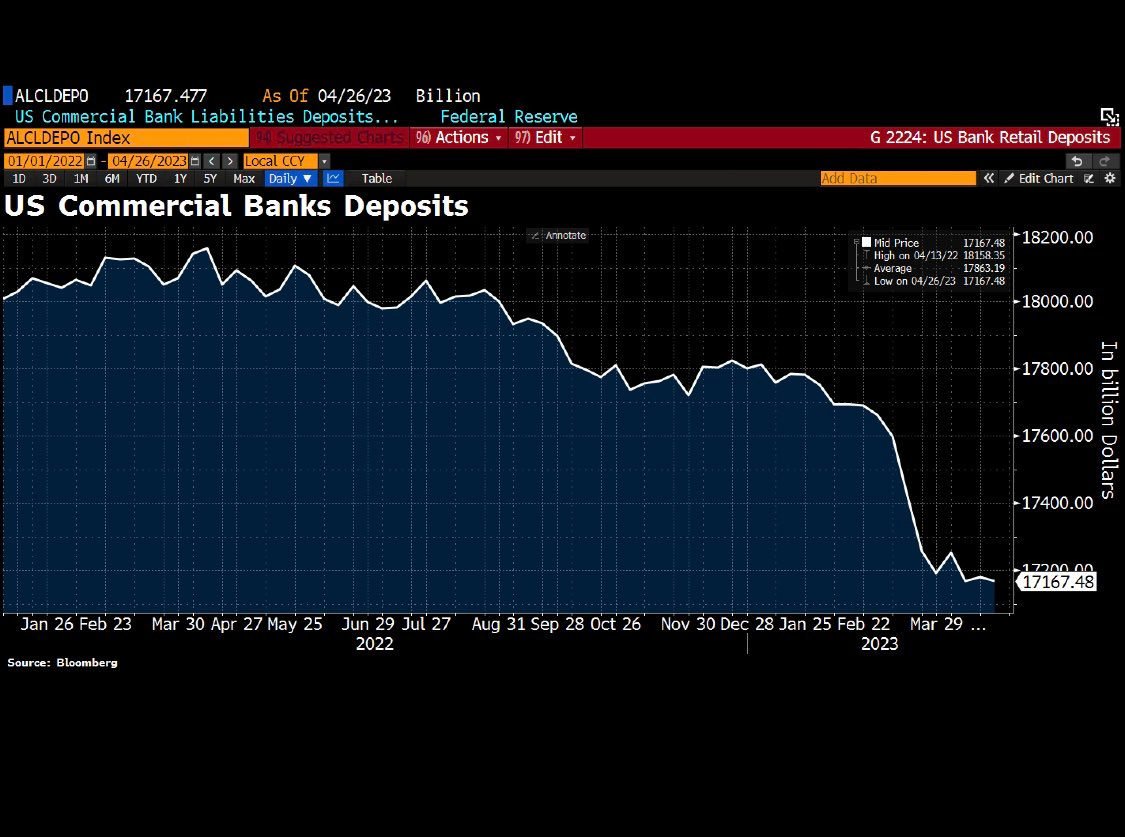

While the media and central bankers are downplaying the financial crisis, and even lying that the banks are solvent, there is basically a slow motion crash and bank run, with a flight of deposits from small to large banks. US Bank deposits fell by $12.5 billion over a recent week, and since the beginning of the Fed rate hikes in March of 2022, there has been almost $1 trillion ($967.5 billion) in bank deposit outflows, the greatest recorded outflow ever. 722 US banks also reported unrealized losses, exceeding 50% of capital, because when Fed rates were close to zero, banks used uninsured deposits to both invest in securities and purchase bonds. However, unrealized losses surged when rates rose.

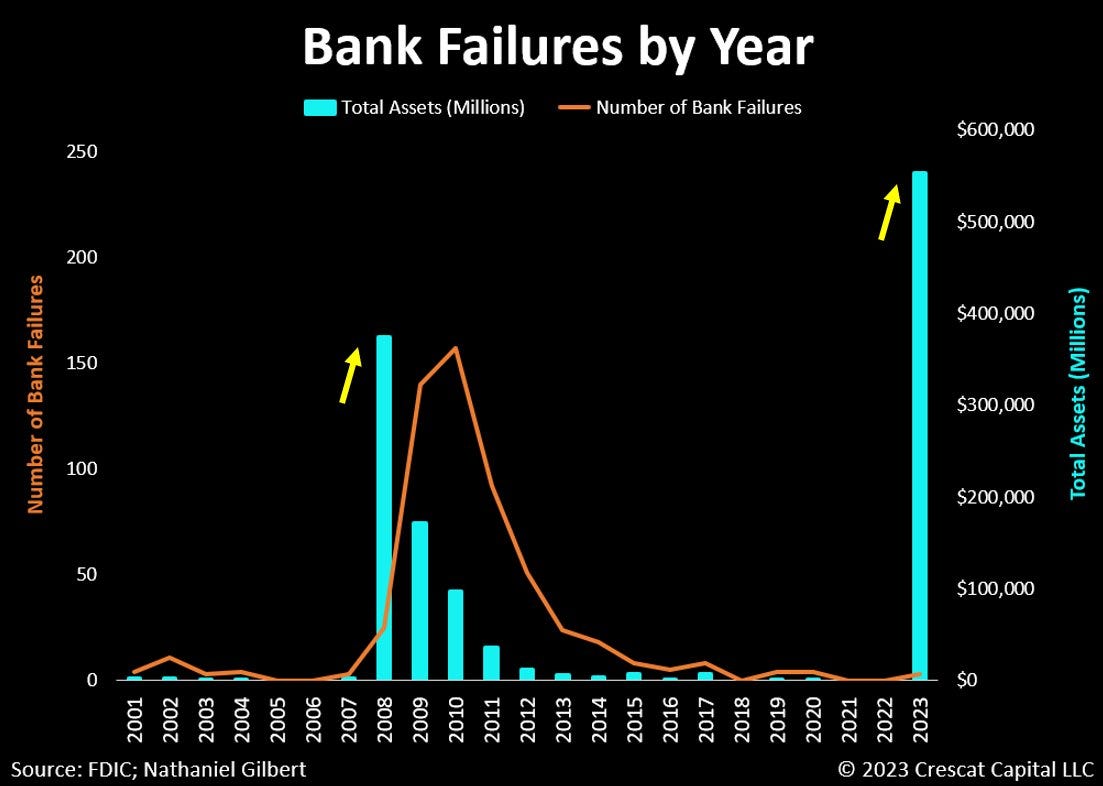

This banking crisis is already worse than the bank failures of 08, with First Republic Bank the 2nd largest bank failure, Silicon Valley 3rd, and Signature Bank the 4th largest in history. Even though 150 banks failed during the Financial Crisis in 2008, this year’s 4 bank failures already equate to nearly the entire amount of assets that financial institutions held during the banking crisis of '08 and '09. There is also a risk of a derivatives tsunami, as 25 large US banks have a whopping $247 trillion in derivatives, including regional banks like First Republic. Warren Buffett called derivatives, financial weapons of mass destruction, that could trigger an implosion of the entire financial system.

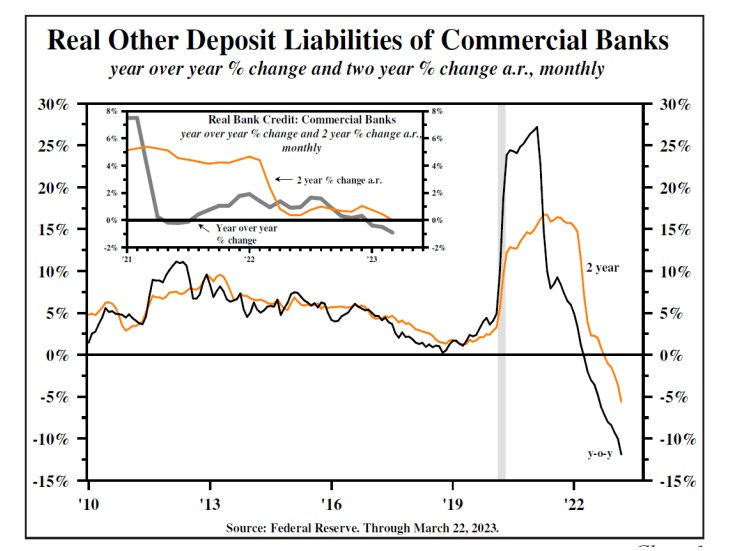

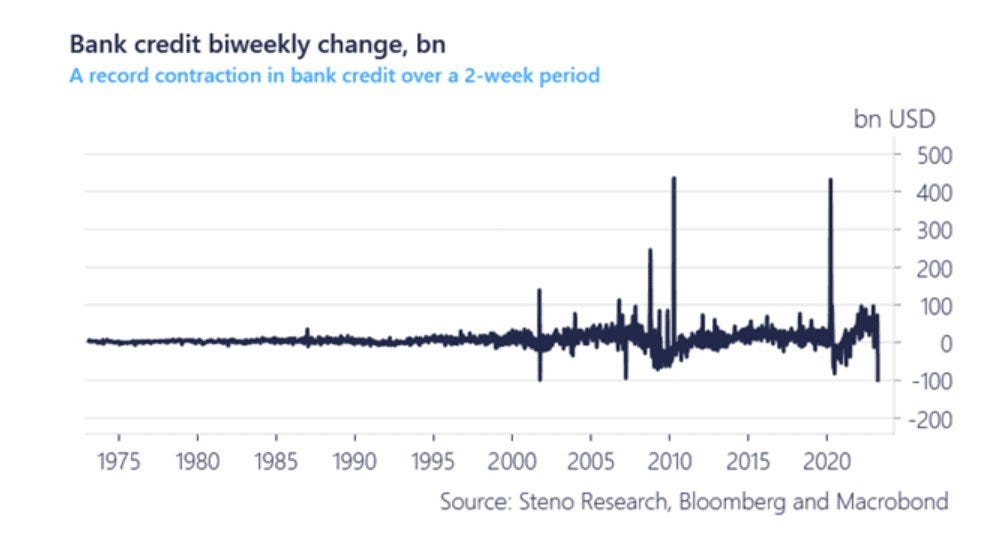

This is just the tip of the iceberg, as even now with very low unemployment, banks are crashing. The commercial real estate crash, credit card debt, and rising unemployment will cause further defaults that will tank the financial system. Even if there is not a dramatic collapse overnight, a likely scenario is greater consolidation of the banking system and the phasing out of smaller banks. Not to mention the inevitable credit crunch, which will guarantee a deep recession, and risk a Depression. For instance, there has been the sharpest decline in the money supply since the 1930s, including bank deposits. This is even taking into account the bailouts. There has also been the 2nd biggest decline in bank lending in US history, with the biggest 2-week decline in bank lending in March, all of which is causing the banking Ponzi scheme to implode. Not to mention the danger of bank bail-ins in the future.

This is blatant corruption and cronyism, such as billionaire depositors at Silicon Valley Bank getting anonymously bailed out, and JP Morgan profiting $2.5 billion from their acquisition of First Republic, arranged by the FDIC, who are also loaning JP Morgan $50 billion. Janet Yellen basically admitted that the bailouts were just for the too big to fail banks, and not for the smaller banks. Prior to the acquisition of First Republic, JP Morgan controlled 15% of US deposits, but after their acquisition, JP Morgan could control 20% of deposits, adding another $100 billion to their deposits. It is notable that JP Morgan also acquired Bear Stearns after the 08 crash. This is government assisted consolidation, the merger of private banks with the State, that is subsidized by the tax payers and depositors with higher bank fees. The financial oligarchy also exploits state regulation to prevent competition in financial markets.

The combination of the credit crunch and destruction of smaller banks could wipe out the majority of small businesses, which are heavily dependent upon regional banks for loans. Consolidation will create a system where only big corporations can get access to credit. With the Fed raising interest rates again by .25 points, I initially took the stance that raising rates was the lesser of evils in order to prevent stagflation. However, one could make the case that the Fed is raising rates to intentionally crush small banks and consolidate the financial system into a handful of too big to fail banks. Not to mention that rate hikes are pushing interest on the national debt to unsustainable levels, and may not even solve inflation. Another reason for the founding of North Dakota’s Public Bank, was in response to high interest rates, as public banks can make low interest loans. Prior to the 08 financial crisis, there were interest rate swaps, which were offered as a protection by banks to absorb the difference in fed rates. However, the rate swaps were a scam, as interest rates were kept low after the 08 crisis, and local governments ate the costs. Many local governments went bankrupt, which is why public banking is more fiscally responsible.

US Greenback

Source: Wikipedia

As for alternatives to the Federal Reserve Banking System, there are the “End the Fed”, Austrian School, Goldbug, Libertarians, and then there are the anti-usury and pro-public banking populists, who want to nationalize the Fed. Libertarians will describe what the government is doing to assist the consolidation of the banking system, as nationalization. However, it muddies the water when Libertarians also compare Public Banking to nationalization. Libertarian financial youtuber types also tend to place blame solely on government and not private bankers, which neglects broader issues of the concentration of wealth and power in the oligarchy, and the financialization of the economy.

The Populist Movement of the late 19th to early 20th Century, including William Jennings Bryan, was in response to a credit crunch, much like the one we are facing now, that also inspired the Wonderful Wizard of Oz book, published in 1900. The money supply shrunk during the Civil War, so Lincoln issued greenbacks to fund the war effort. However, silver coins were demonetized in 1873, paving the way for the Gold Standard. This radically shrunk the money supply and caused a Depression. Banks could call in loans at will, if they did not have backing, and farmers, who had taken out loans, lost their farms. This narrative seems at odds with the Libertarian Goldbug view that a Gold Standard is needed to prevent inflation, and most of these populist figures, like William Jennings Bryan, opposed the Gold Standard, but supported free silver. Economists focus on the Great Depression and 70s stagflation, but often overlook these panics of the late 19th Century.

Ellen Brown is also very critical of the Gold Standard, because it would make it difficult for people to have access to credit. Ellen Brown’s solution for inflation is replacing private banks issuing debt with the State issuing debt free greenbacks, like Lincoln did during the Civil War, which did not cause hyperinflation. Ellen Brown references the recommendations for the economy and inflation of economist, Prof. Richard Werner, who suggested that “banning bank credit for transactions that don’t contribute to GDP; creating a network of many small community banks lending for productive purposes, returning all gains to the community; and making bank behavior transparent, accountable and sustainable.” Ellen Brown also supports debt free local currencies.

Libertarians would still criticize these proposals as inflationary, such as Libertarian, Austrian, Gary North, dismissing Ellen Brown’s ideas as Keynesian and Statist. Libertarians would also view populist, social credit dividends, as the same as Modern Monetary Theory. Ellen Brown has actually expressed sympathy towards Modern Monetary Theory. However, former congressman, Ron Paul, who is an Austrian and a Libertarian icon, vindicates Ellen Brown, in proposing the State issuing greenbacks or a new special currency for the purpose of paying down the deficit. This would not cause inflation, because the greenback or special currency would not be in circulation. China, South Korea, Japan, and Argentina have done this in the past, so has Qaddafi in Libya, and more controversially, Hitler did in response to Weimar inflation. It is important for people to know that there are alternative or third way economics, besides just tax and spending, inflation causing printing, and conservative and libertarian proposals for austerity, to deal with inflation and the debt ceiling.

There is going to be a rebuilding of the financial system after the crash, a “Great Reset” if you will. Unfortunately, most smaller regional banks will crash and little will be done by the Fed to save them. However, there are opportunities for local jurisdictions, such as cities and counties, to take initiative to create new public banks, without needing to rely upon the State or Federal Government. With economic devastation of rural and deindustrialized communities, public banks can bring back wealth and take care of the local economy. Public banks can also address the unique economic needs of specific regions, from farming to tech, that mega banks are not able to. There should be a decentralized network of smaller regional public banks, that assist credit unions, private banks, local economies, and small business. The question is whether there can be a truly decentralized financial system, that is reliant upon neither the Fed and its monetary controls via interest rates, or mega banks.